Openings we see, closures we don’t

Our major grocery chains continue to open and convert discount stores across the country. Metro recently announced plans to open about a dozen new locations in 2026, focusing primarily on expanding its discount brands, including Super C and Food Basics. This week, Loblaw — the country’s largest food retailer — followed with its own announcement: a $2.4-billion investment in 2026 to open roughly 70 new stores across Canada, including Shoppers/Pharmaprix pharmacies and No Frills/Maxi discount grocery outlets, while renovating nearly 200 existing locations.

Every year, we witness the same choreography of announcements: new store openings from coast to coast. More stores to serve a market that claims to crave competition. More stores, more choice, lower prices — right?

At first glance, the news sounds encouraging. But the data tell a different story.

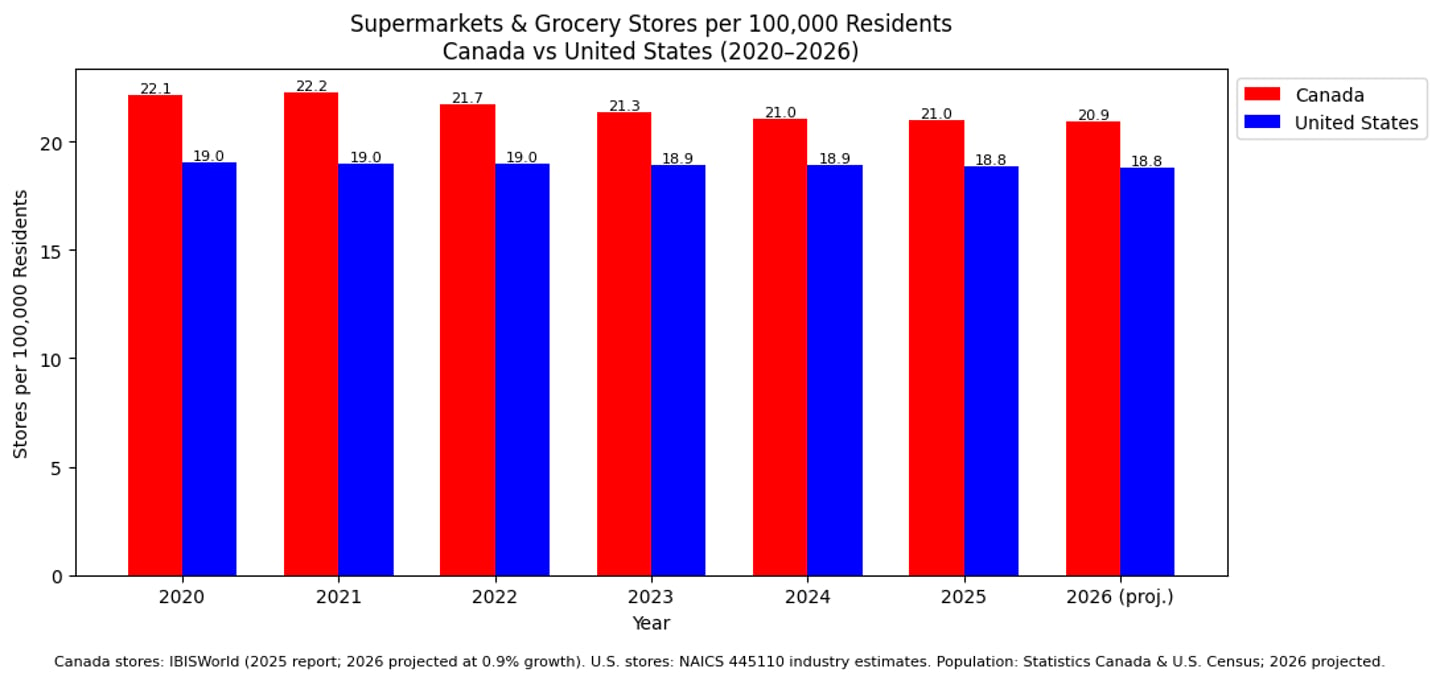

According to IBISWorld, Canada had 8,801 supermarkets and grocery stores at the end of 2025 — excluding specialty shops and convenience stores. That represents 21.0 stores per 100,000 residents. In 2020, the figure stood at 22.1 per 100,000. That is already a decline. Based on current projections, the ratio will fall further to 20.9 in 2026 — a 5.4% decrease since 2020.

A comparison with the United States offers some comfort — at least superficially. In 2020, the U.S. had 19.0 supermarkets per 100,000 residents. By 2025, that number had edged down to 18.8 and is expected to remain stable in 2026 — a decline of barely 1%. In other words, while Canada is experiencing a noticeable contraction in store density, the ratio south of the border has remained largely unchanged.

Comparing North America with Europe is more complex. Europe’s agri-food economy is far more regionalized, and retail there is built around proximity and walkability. In North America, our retail model still depends heavily on automobiles and long travel distances.

What is particularly frustrating about these early-year announcements is what they leave unsaid. We are told how many stores will open — but never how many will close at the same time. That missing piece of information is critical to understanding the real evolution of the market. It is, quite frankly, an optics issue. Loblaw disclosed closures several years ago, and the public reaction was far from positive.

Determining the optimal number of supermarkets in a country as vast as Canada is not straightforward. Renewal and modernization of the store network are certainly welcome. And as Canada’s population growth slows, we can reasonably expect stabilization — perhaps even rationalization — in the number of supermarkets nationwide.

READ: Why depopulation is the food industry’s silent crisis

That does not necessarily mean fewer choices for consumers. There is still room for smaller players and independents who quietly differentiate themselves across the country by offering something distinct. A declining store-per-capita ratio does not automatically imply a shrinking food offer. It simply means there are fewer large-format stores per Canadian than there were five or six years ago — an important nuance that triumphant press releases tend to obscure.

In food retail, as in economics, context matters far more than headlines.