The economy is sluggish. So why is fast food struggling?

For decades, economic slowdowns followed a predictable script in foodservice. As household budgets tightened, consumers traded down. Full-service restaurants suffered. Fast food thrived. Value, convenience, and predictability made quick-service restaurants (QSRs) the natural refuge in uncertain times.

That script no longer holds.

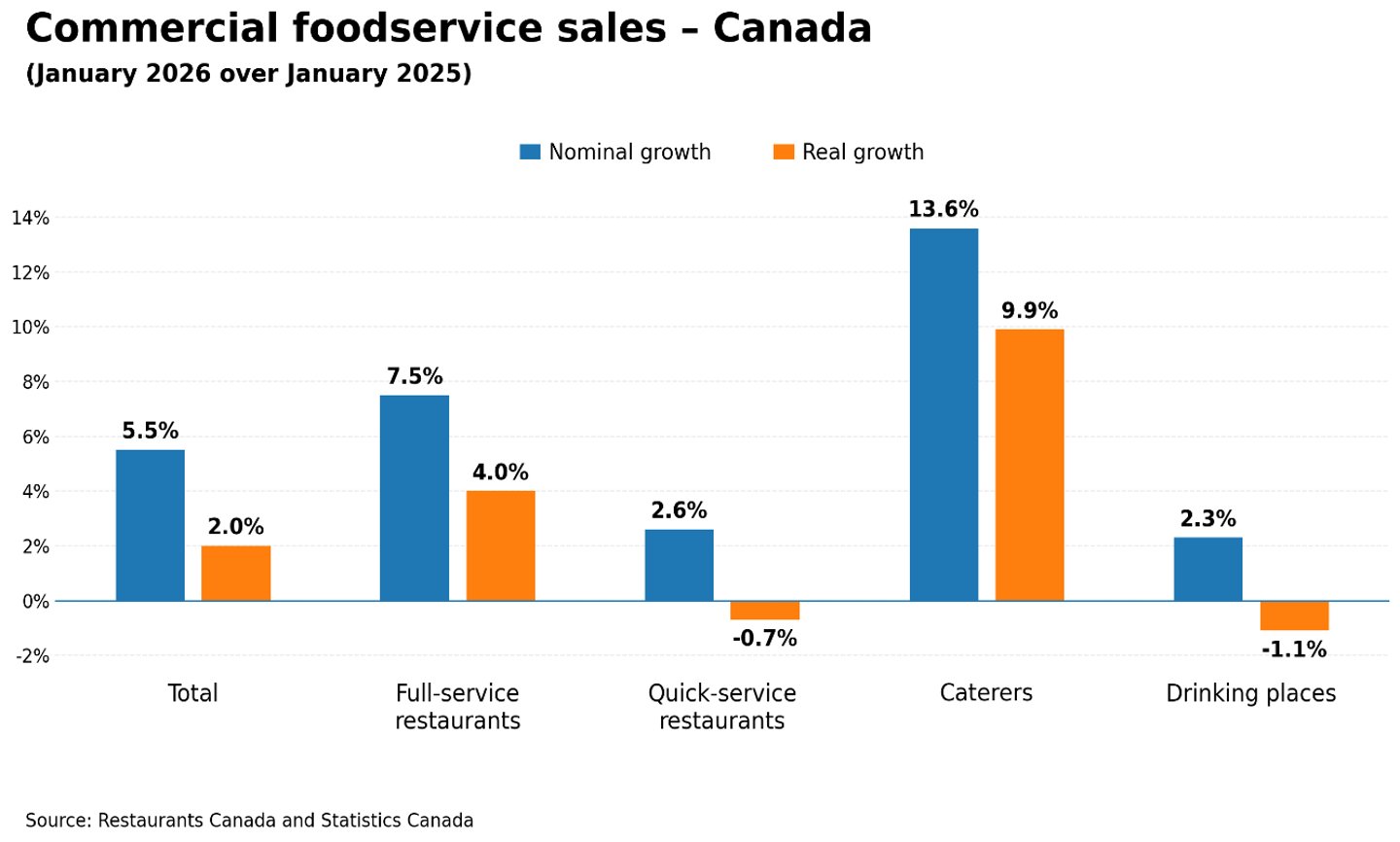

New data from Restaurants Canada and Statistics Canada show that while overall foodservice sales are still growing in nominal terms, the story changes once inflation is removed. Real growth—what actually reflects volume and traffic—is now negative for quick-service restaurants. In other words, Canadians are spending more at fast food chains, but they are buying less.

This is not a cyclical blip. It is a structural shift.

The core issue is simple: fast food has lost its value proposition. Over the past few years, QSR operators have aggressively raised prices to offset rising input costs—labour, energy, ingredients and logistics. In doing so, they have crossed a psychological threshold. What was once perceived as an affordable option is now, for many households, anything but.

READ: Canada is poised to lose 4,000 restaurants in 2026. Does anyone care?

A combo meal that used to cost under $10 can now easily exceed $15 in many markets. For a family, that difference is not trivial. It is decisive.

Consumers have responded accordingly—not by trading down into fast food, but by exiting the category altogether. Increasingly, the real competition for QSR is not other restaurants, but grocery stores. Retailers have adapted quickly, offering ready-to-eat meals, hot counters, meal kits and aggressive promotions. For many households, the grocery store now delivers better value per dollar than fast food.

READ: Consumers crave more from home-meal replacements

This shift has fundamentally altered the “trade-down” pathway. It used to be: full-service to quick-service. Today, it is more often: restaurants to retail.

At the same time, the broader economy is becoming more polarized. Higher-income households—less sensitive to inflation and interest rates—continue to support full-service dining. This helps explain why sit-down restaurants are still showing positive real growth. Meanwhile, the core customer base of QSR—working and middle-income Canadians—is under sustained financial pressure. Rising housing costs, elevated interest rates, and persistent food inflation have eroded purchasing power. Frequency is down. Basket sizes are shrinking. In some cases, visits are being skipped entirely.

Quick-service restaurants are, in effect, being squeezed from both ends. They are no longer cheap enough to dominate the value segment, and not differentiated enough to compete with premium dining experiences.

The result is what we are now observing: negative real growth in a segment that has historically been recession-proof.

This also helps explain the recent resurgence of aggressive value strategies, including $5 meal offerings from major chains like McDonald’s. These are not mere promotions. They are corrective measures. When traffic declines, margin discipline becomes secondary to volume recovery. Restoring price credibility is now essential.

But regaining consumer trust will not be easy. Once a value brand loses its positioning, it takes time—and consistency—to rebuild it.

The implications extend beyond fast food. What we are witnessing is the erosion of the middle in foodservice. High-end dining is holding. Event-driven catering is thriving. But the everyday, accessible segment—the one that serves millions of Canadians each week—is under strain.

This should concern policymakers and industry leaders alike. Foodservice is not just about meals; it is a key employer, a driver of urban vitality, and a barometer of household financial health.

If fast food can no longer play its traditional role as the affordable fallback option, then the pressure on households is more severe than headline inflation numbers suggest.

The data are clear: consumers have not stopped eating out. They have become far more selective about where—and whether—they spend.

Fast food, it seems, is no longer the default choice in tough times.

And that changes everything.